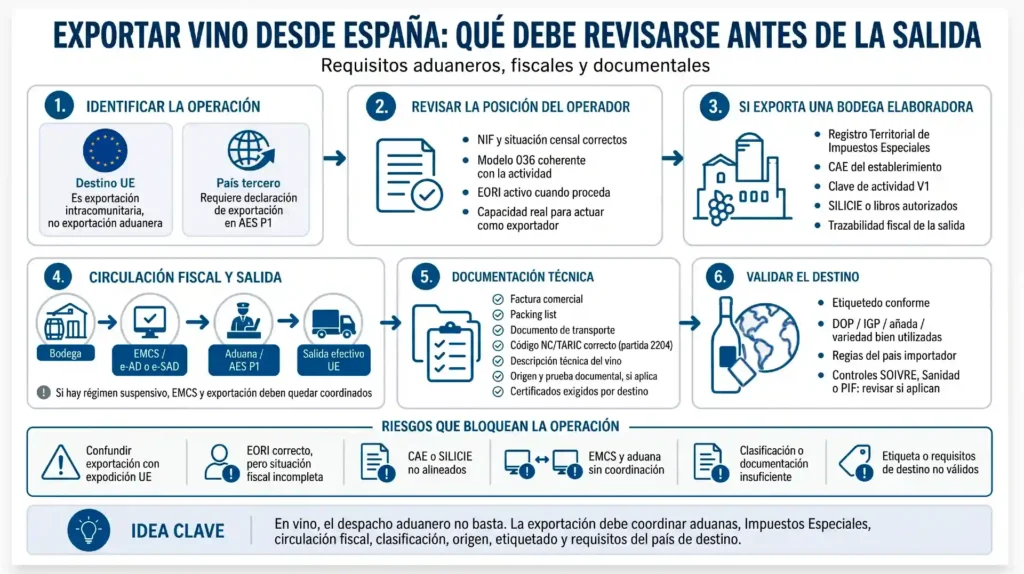

Exporting wine from Spain requires reviewing the operation before preparing the goods.

The first risk arises when confusing an export to a third country with an intra-EU dispatch within the European Union.

The second risk lies in treating wine as an ordinary commodity, ignoring its connection with Excise Duties, the Territorial Register, CAE, SILICIE, fiscal circulation, origin and labelling.

For winemaking cellars, the critical point is not only having an EORI number for customs clearance, but also proving that the wine’s exit is consistent with the fiscal status of the establishment.

A commercially closed transaction may be blocked if the customs, tax and regulatory documentation is not aligned.

This article explains what must be verified before exporting wine from Spain and when a customs specialist should become involved.

In international trade, the expression “exporting wine” is used for any sale outside Spain. Technically, this wording is not always correct. A sale of wine from Spain to France, Germany, Italy or Portugal is not a customs export, but an intra-EU operation. A customs export exists when the wine leaves the customs territory of the Union for a third country.

This distinction is not merely formal. It affects the customs declaration, VAT, transport documentation, the circulation of products subject to excise duties and proof of exit. For exports to third countries, the AEAT (Spanish State Tax Administration Agency) requires the use of the AES P1 electronic export system, which is enabled for submitting declarations that include goods under the export procedure.

The usual mistake is to prepare the operation based on the invoice and transport, without first reviewing whether the cellar or exporter is correctly positioned before the AEAT. In wine, that review must go beyond the EORI number. If the exporter is a winemaking cellar, its position regarding Excise Duties, its Territorial Register, its CAE, its SILICIE obligation and the way the movement is reflected in the establishment’s fiscal accounting must be analysed.

Wine is included in the Tax on Wine and Fermented Beverages. Although Law 38/1992 establishes a zero tax rate for this tax, the BOE itself states that the tax makes it possible to structure the circulation system applicable to producers of wine and fermented beverages.

Therefore, the risk does not disappear because the tax rate is zero. The risk arises when the cellar cannot properly justify the production, holding, exit and destination of the wine.

Before preparing documents, the legal destination of the goods must be determined.

If the wine is sent to a country outside the customs territory of the Union, the operation requires a customs export declaration. In Spain, this declaration is processed through AES P1. The AEAT identifies AES P1 as the electronic system enabled for submitting customs export and outward processing declarations.

If the wine is sent to another Member State of the European Union, no customs export declaration is submitted. In that case, intra-EU VAT, VIES/ROI, proof of transport and the fiscal circulation of the product must be reviewed, but an export clearance is not processed as it would be for a shipment to a third country.

Failing to separate these two scenarios causes documentary errors from the outset. A correct invoice does not fix an incorrectly classified operation.

The operator must be correctly registered in the Census of business owners, professionals and withholding agents when carrying out an economic activity. The AEAT establishes that those required to be included in this census must submit a registration declaration using Form 036, and must also use it for amendments or deregistration.

In a wine export, the following must be reviewed:

If the operator is already registered, a new registration may not be necessary, but a census review may be. The declared activity must be consistent with the actual operation.

In a wine export, the EORI allows the exporter to appear in the customs declaration. But it does not, by itself, validate the fiscal situation of a winemaking cellar. That point must be dealt with separately.

When the operator is a winemaking cellar, the main analysis must shift to Excise Duties.

The Territorial Register for Manufacturing Excise Duties applies, among others, to the Tax on Wine and Fermented Beverages. The AEAT includes holders of factories, tax warehouses and fiscal warehouses among those obliged to register, and reminds operators that, if there are two or more activities or establishments, registration must be requested for each one.

In an export carried out by a winemaking cellar, it must be verified:

It is not enough for the company to sell wine. It must be able to justify that the wine leaves from a properly identified and controlled establishment.

The CAE identifies the authorised establishment for Excise Duty purposes. In the case of an establishment authorised as a wine producer, the AEAT indicates that the eighth and ninth characters of the CAE are V1.

This information is key in wine exports because it makes it possible to check whether the establishment is authorised for the activity it declares it carries out.

There must be consistency between:

If the wine physically leaves a cellar, but the invoice, exporter, CAE or fiscal documentation refer to different operators without documentary justification, the operation is exposed to incidents.

The AEAT establishes that an establishment authorised as a wine producer is a factory and, therefore, is subject to SILICIE, unless it is authorised to keep Excise Duty accounting through folio-numbered paper books.

SILICIE is not an ancillary procedure. It is the Excise Duty accounting system that enables control over movements, operations, processes and stock.

When the cellar directly submits the entries through the AEAT Electronic Office, the submission must be made within twenty-four working hours following the movement, operation or process. The AEAT also provides for specific deadlines when the submission is made from the taxpayer’s computerised accounting system.

Before exporting wine, it must be checked:

Control is not limited to payment of the tax. Control affects the fiscal traceability of the wine.

The wine may leave the cellar and circulate to a port, airport, warehouse, depot or exit point. This movement must be analysed from an Excise Duty perspective.

The EMCS system documents movements of products subject to Excise Duties by means of an electronic administrative document, e-AD, for goods under duty suspension, or by means of a simplified electronic administrative document, e-SAD, for movements where duty has been released for consumption.

In exports involving products subject to Excise Duties under duty suspension, the customs documentation and EMCS documentation must be connected. The European Commission’s AES guide indicates that, if an export contains goods under Excise Duty suspension, the e-AD must be declared in the export declaration through the corresponding information, including the ARC and UBR as a previous document.

Therefore, the review must confirm:

A wine export should not be prepared only with an invoice, packing list and transport. The fiscal circulation must match the clearance.

The tariff classification must be determined before submitting the declaration. Wine of fresh grapes, including fortified wines, falls under heading 2204, but the four-digit heading is not sufficient to declare correctly.

The applicable subheading must be specified according to:

Classification affects the export declaration, TARIC measures, statistics, origin, certificates and destination country requirements. A generic description such as “red wine” or “white wine” is not a sufficient technical basis for validating an export.

When the wine leaves for a third country, the export declaration must be processed in AES P1. The declaration must be built with consistent data, not approximate information.

At a minimum, the following must be consistent:

The customs declaration should not be used to correct a poorly prepared operation. It must reflect an already validated operation.

If the importer requests tariff benefits at destination, it must be checked whether an applicable preferential agreement exists and whether the wine meets the corresponding rule of origin.

Access2Markets reminds users that, for preferential tariff treatment to apply, origin must be proven to the authorities of the destination country. The type of proof depends on the applicable agreement and may consist of an exporter’s declaration, a certificate of origin or importer’s knowledge.

Simply stating “origin Spain” on the invoice is not enough. Documentary evidence must exist to defend that origin.

REX is not a general registration for exporting wine. It should only be reviewed when the applicable preferential agreement allows or requires it for issuing statements on origin.

Wine is not a generic food product. It may be linked to designations of origin, protected geographical indications, traditional terms, vintage, variety, lot, bottler, alcoholic strength and mandatory indications.

Commission Implementing Regulation (EU) 2019/34 develops rules related to protected designations of origin, protected geographical indications, traditional terms and controls in the wine sector.

In addition, since 8 December 2023, new European Union rules on the indication of ingredients and nutritional values for wines and aromatised wine products have applied, with a regime applicable to wines and wine products obtained from the 2024 harvest onwards and an exception for wines produced before 8 December 2023 until stocks are exhausted.

For exports to third countries, the regulations of the importing country must also be reviewed. Access2Markets warns that countries often impose detailed packaging and labelling requirements, whether mandatory or voluntary, and that the specific requirements of the import market must be checked.

A label that is valid in Spain does not guarantee automatic admission in the United States, the United Kingdom, Mexico, China, Japan, Canada, Switzerland, the United Arab Emirates or any other third country.

Before loading the goods, Omnia Aduanas must validate:

The documentation must be prepared and the risks corrected before the wine leaves Spain.

Exporting wine from Spain requires a prior technical review. Customs clearance is only one part of the operation. For winemaking cellars, the critical point lies in coordinating customs with Excise Duties: Territorial Register, CAE, SILICIE, fiscal circulation and traceability of the exit.

The error does not usually appear when the invoice is issued. It appears when the goods are already prepared, transport has been arranged and the fiscal or customs documentation does not allow the operation to be defended.

A cellar may have an EORI and still not have properly resolved the fiscal side of the export. It may also have product ready for sale and lack a valid label for the destination, defensible proof of origin or a circulation document consistent with the customs declaration.

Omnia Aduanas intervenes before the operation becomes compromised. It reviews the operator’s position before the AEAT, the cellar’s situation regarding Excise Duties, tariff classification, export documentation, fiscal circulation, origin, labelling and the destination country’s requirements.

Before closing an international wine sale, it is advisable to submit the operation to a technical analysis. Contacting Omnia Aduanas makes it possible to confirm whether the export is viable.